Facts:

- This month’s unemployment rate decreased from 4.8% to 4.6%. Unemployment was at 6.3% in January 2021.

- PMI (Purchasing Managers Index) continued to expand (any reading above a score of 50 means expansion). This month’s reading came in at 61.1, compared to last month’s 60.8.

- The S&P 500 (C Fund) increased 7% in October, compared to the 4.65% decrease in September. S&P 500 is up 24.02% YTD.

- The first estimate of Q3 GDP shows growth of 2%, compared to Q2’s reading of 6.7%.

- The Fed Funds interest rate remained at 0.15%.

- The G Fund rate for November was set at 1.625%.

Assessment:

Inflation:

So, inflation was announced as 5.9%, right?

Between December 2019 and August 2021, the U.S. money supply grew by $5.5 trillion, which is a 35.7% increase. See HERE. Theoretically (although not precisely), this should translate to the value of the dollar decreasing by 35.7%. Which it almost already has! See the infographic below, and the source site HERE.

And that’s without factoring in the anticipated increase in U.S. money supply.

The Federal Reserve’s expected purchases of Treasurys and mortgage backed securities, estimates forecast that the money supply will grow another $5.1 trillion by the end of 2024.

That’s $10.6 TRILLION in new money.

Now, not all $10.6 Trillion will stay within the economy. Only an expected $8.2 trillion. Still, $8.2 trillion represents a 53.2% increase in monetary supply by 2024. That translates into 53.2% decline in the value of the dollar between 2019 and 2024.

This is going to have real effects, most dramatically amongst those who are not seeing wage increases rise with inflation – which is most of the economy. See HERE.

Bottom Line:

I am sorry to say that both G fund and F fund are poor options in this environment. G fund is under-performing inflation (inflation is 5.9% while G fund is 1.635%). F fund is exposed to interest rate risk. Inflation leads to a rise in interest rates which will crush the F fund.

Of the two, the G fund is the lesser of the two evils, because the F fund will have a double-whammy: It’ll lose principle and the remaining principle will be deflated, meaning less valuable. G fund can’t lose principle.

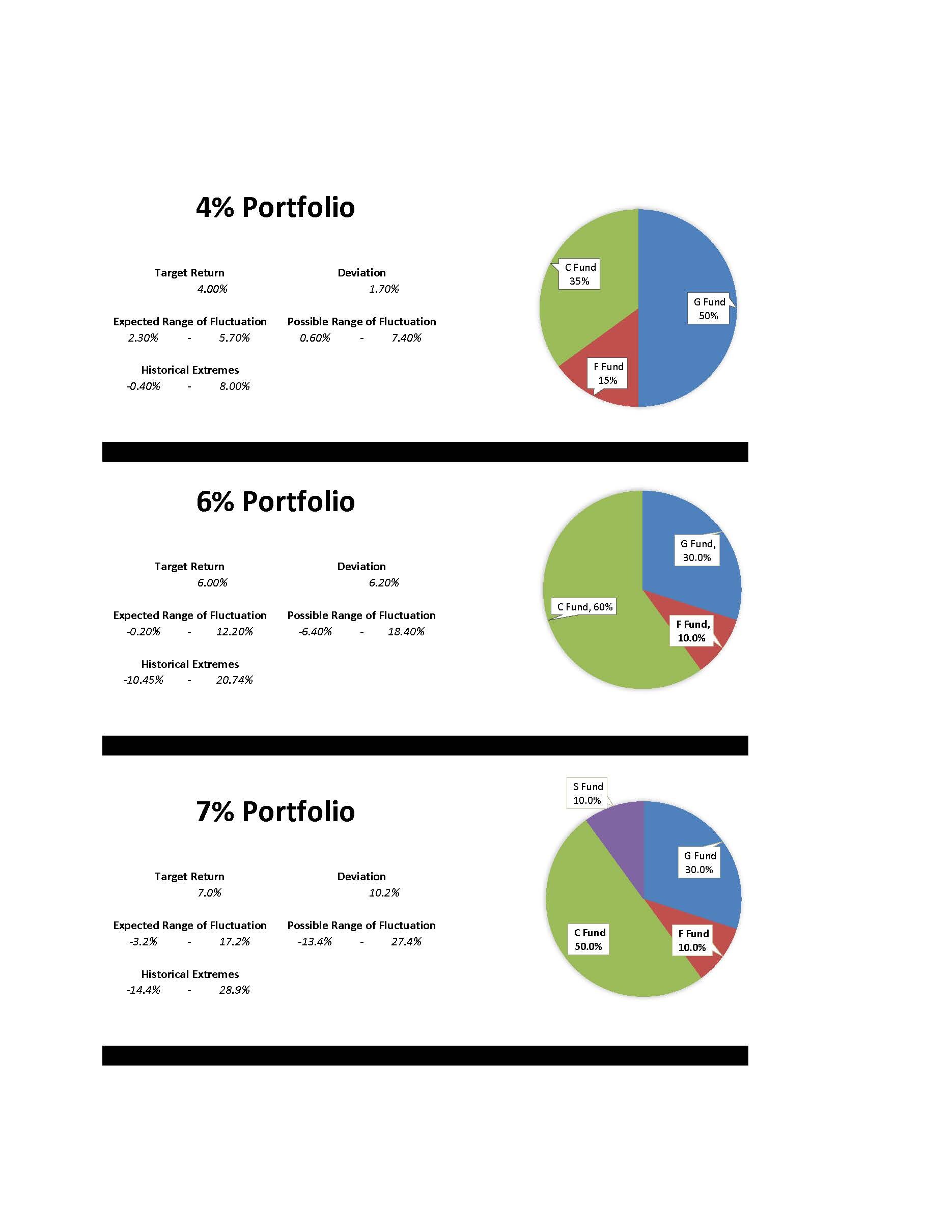

See this month’s recommended portfolios. DON’T JUST LOOK AT RATE OF RETURN. Always view the target return of each portfolio in context of its ranges of fluctuation.

Anyone who has more than 5 years before drawing income from their TSP should consider taking a more aggressive posture going forward and use my aggressive portfolio’s below. If you are within 5 years of retirement, you should email me to get a more customized recommendation.

If you have any questions, feel free to contact me.

Email me here – stephen@stephenzelcer..com