TSP Report November 2023

Facts:

- The G Fund rate for November 2023 increased to 5%. Wow!

- The Fed Funds interest rate decreased slightly from 5.5% to 5.3%.

- This month’s unemployment rate increased from 3.8% to 3.9%.

- The 2nd Estimate for Q3 GDP came in at 5.2%. Last quarter’s GDP was 2.1%.

- PMI (Purchasing Managers Index) contracted to 49.4 (any reading below 50 represents contraction).

- The S&P 500 (C Fund) decreased 2.1% in October. Thus far in November, S&P 500 is up over 8%. YTD, S&P500 is up 19%.

Assessment:

World War III?

Well, it seems the markets have shrugged off the threat of war, with November being the best month of the year for the C fund, thus far.

Last month I showed the historical data that shortly after wars begin, the markets recoil. That didn’t really happen with this Hammas-Israel war.

Three months ago I highlighted the looming Defaults.

I gave the following illustration:

Typical commercial real estate loans have a 5-yr term. That means, in 5-yrs they need to be either satisfied or refinanced.

However, when it’s time to refinance, instead of holding a 4% mortgage from 2018, they are forced to refinance into an 8%+ mortgage in 2023. That, by itself, is a challenge. However, it gets worse.

Commercial real estate values have declined. A building that was bought for $10M in 2018, may now be worth $8M in 2023. Assuming a 20% LTV, the loan on that original $10M property was $8M. When it comes time to refinance, if the property is now valued at $8M, the LTV would only allow a loan of $6.4M. That means the property owner needs to somehow find $1.6M of cash just to refinance the original $8M loan.

When confronted with this decision – either cough up another $1.6M and refinance into costly 8%+ loans, or cut your losses and walk away – it’s not hard to foresee many owners walking away from their loans, and defaulting.

Possible lowering of interest rates:

We have an election year coming up, and lowering interest rates is a tactic that politicians can use to buy votes.

Also, there’s speculation that inflation may have reached containment, in which case the fed can ease up on the interest rates, but only slightly.

If the Fed reduces rates only slightly, it doesn’t really mitigate the above default concerns. However, if there’s a substantial drop of a full percentage, that could stave off a default.

I wish I had a crystal ball.

Bottom Line:

I am confident in the power of companies to make profits. The near term may have bumps, but so long as government doesn’t interfere with markets, the economy will thrive and the market will continue to rise.

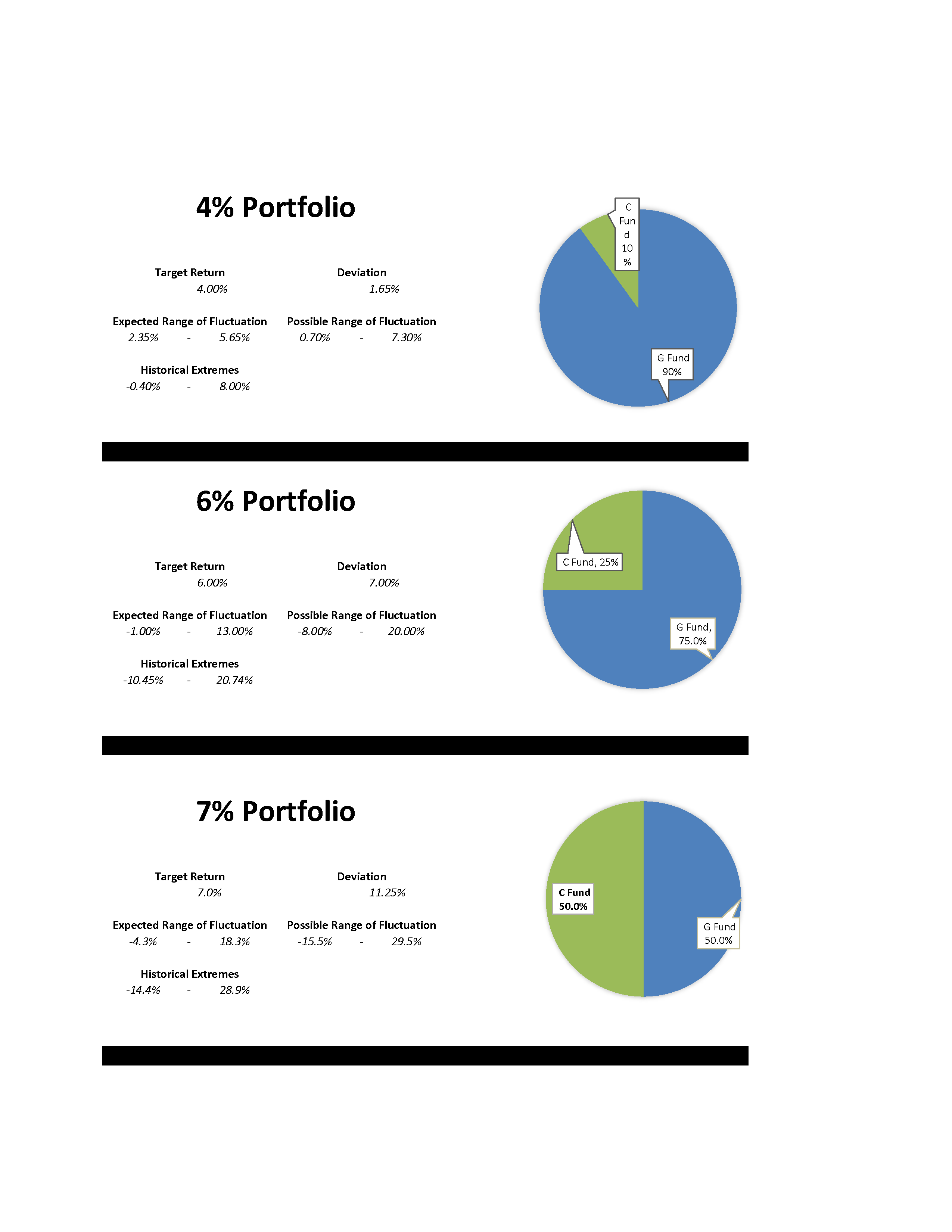

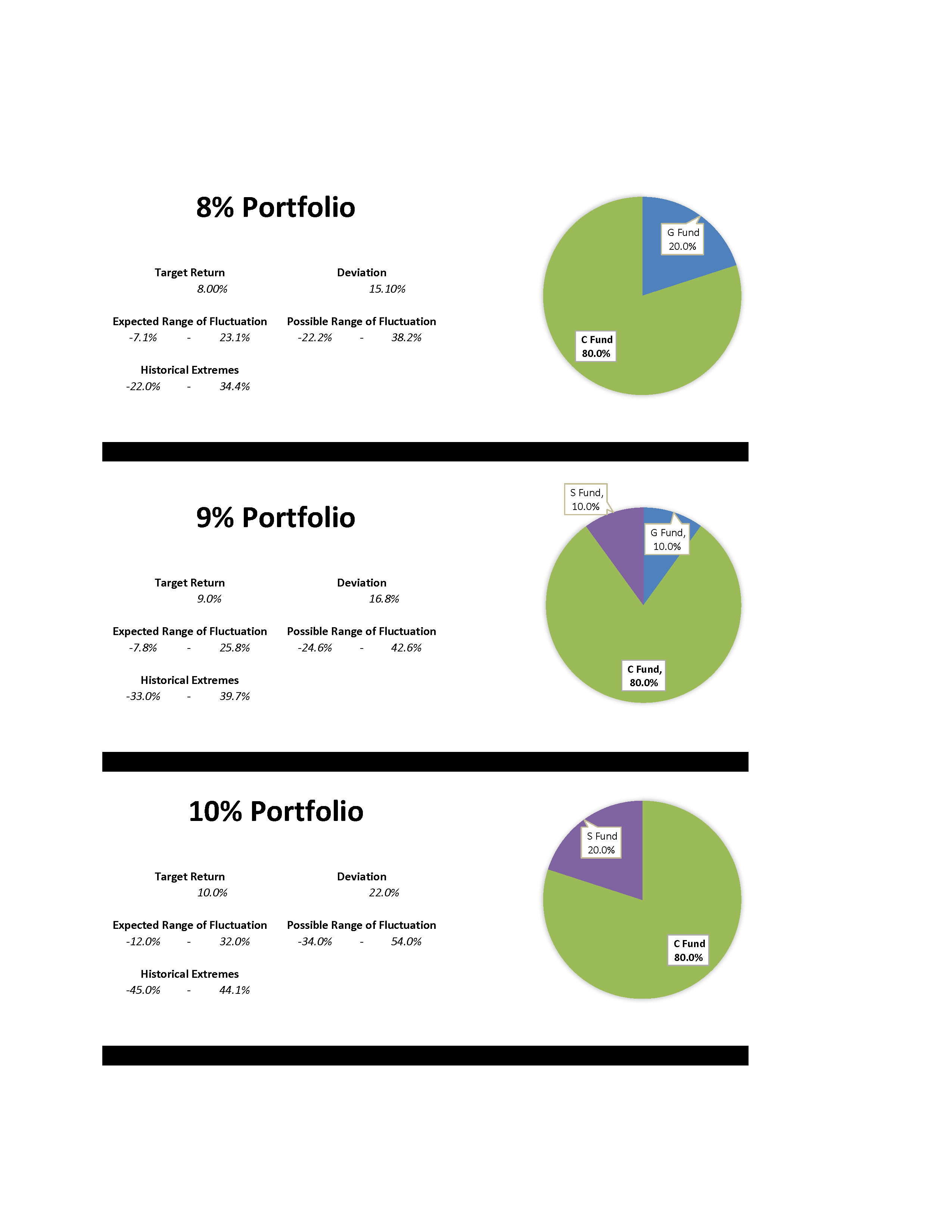

See this month’s recommended portfolios. DON’T JUST LOOK AT RATE OF RETURN. Always view the target return of each portfolio in context of its ranges of fluctuation.

Anyone who has more than 5 years before drawing income from their TSP should consider taking a more aggressive posture going forward and use my aggressive portfolios below. If you are within 5 years of retirement, you should email me to get a more customized recommendation.

If you have any questions, feel free to contact me.

Email me here – stephen@stephenzelcer.com