July 2024 TSP Planning Report:

Facts:

- The G Fund rate for July 2024 decreased from 4.75% to 4.625%!

- The Fed Funds interest rate remained at 5.3%.

- This month’s unemployment rate increased from 3.9% to 4%.

- The 3rd Estimate for Q1 2024 GDP dropped from 1.6% to 1.4%. Last quarter’s GDP was 3.4%.

- PMI (Purchasing Managers Index) expanded, reading at exactly 51.3 (any reading below 50 represents contraction, any reading above 50 represents expansion, a reading of 50 means no expansion or contraction).

- The S&P 500 (C Fund) increased 3.5% in June 2024. Thus far in 2024, S&P 500 is up 15.29% YTD!

Assessment:

Jobs or no jobs?

According to the latest jobs report, June saw a solid 206,000 of new jobs created. This seems like good news! But, as with all stats, if you investigate them, you’ll see it’s not the full picture.

As JP Morgan points out, ¾ of those new jobs were healthcare and government jobs. This is not healthy for the economy, as we’ve discussed before. The reason why it’s not healthy is as follows: When a commercial enterprise creates new jobs, it means the company is being more profitable. A company that is not being profitable can’t afford to hire more people. However, when the government is creating new jobs, it’s not because they are being profitable – they’re not in the business of profit. So how can the government afford to offer new jobs? They either tax the populace, or they print money – both of which hurts the populace.

- Taxes hurt the wallet of the people who pay the taxes – meaning Person A loses money so Person B receives a salary. How ironic. Furthermore, since Person A paid taxes, they have less money to buy a new couch, a new dress, a family vacation – which means the couch seller, dress seller, vacation seller have all lost money. So, the Government “creating” jobs just means we stimulate one person’s finances by hurting other people’s finances. Here’s a good article that explains this basic economic outcome.

- Printing money just causes inflation. We’re all painfully familiar with that.

So, if unemployment is staying level because the government is “creating” jobs, this is simply going to help one segment of the US economy by stifling another part (or many parts). The American people will end up paying for these new jobs in the form of taxes or inflation – both of which put even more pressure on the already-suffering cashflow.

Furthermore, even though jobs are seemingly being “created,” they’re not being filled! That’s why the unemployment numbers increased! Or, as JP Morgan points out, even if some people are being hired, there’s more people losing jobs in other sectors.

As CNN reports – The services sector of the economy – meaning the sector providing services as opposed to goods – is weakening. One of the metrics of weakness is the degree of demand. PMI (Purchasing Manager’s Index), which is a measure of demand, showed that while overall economically there’s slight expansion (51.3), the PMI for service-based businesses, specifically, contracted from 54.1 to 47.3. This is significant because, as CNN points out, 86% of US jobs are service-based! That means the largest sector of work is shrinking!

Why is it shrinking? The assumption, as pointed out in the article, is people’s wallets are still feeling pinched by inflation and people are really tightening their belts.

You know who else is tightening?

Banks are tightening on lending:

Regional banks are tightening up lending. This was expected because banks are losing their primary sources of funds (for lending):

- Payoff of Existing Loans

- Cash Deposited with the Bank

Both of these are suffering:

Payoff of Existing Loans-

Only a fraction of existing loans are being paid off, mostly because previous loans have a much more favorable interest rates than what’s currently being offered. This incentivizes borrowers to extend their current loans rather that payoff previous loans. Additionally, loans on properties are often paid off when a property is sold. Currently, there are much fewer transactions occurring in real estate and thus much less payoffs.

Cash Deposited with the Bank-

Bank deposits are also suffering as individuals and businesses are taking their funds out of checking or savings accounts for two reasons:

- Higher yields elsewhere: Why should clients keep their money in a bank account yielding 1% when money markets are yielding 5%?

- Clients just have less cash due to inflation eroding their savings and cashflow.

Both of these impact the funds a bank has to lend and, thus, banks are tightening their lending.

Bottom Line:

There are many arguments to say the market will be pushed downward for the foreseeable future. The only bright spots are:

- It’s an election year, and lowering interest rates is in the interest of an incumbent to boost their re-election bid.

- Companies have a vested interest in making profits. In general, I am confident in the power of companies to make profits, and if they do, the economy will thrive and the market will continue to rise – so long as Governments don’t interfere.

It’s important to remind ourselves – the economy has been stagnating for months and yet the S&P500 is up over 15% YTD!!! So, we can never say with certainty when a crash or spike is going to happen.

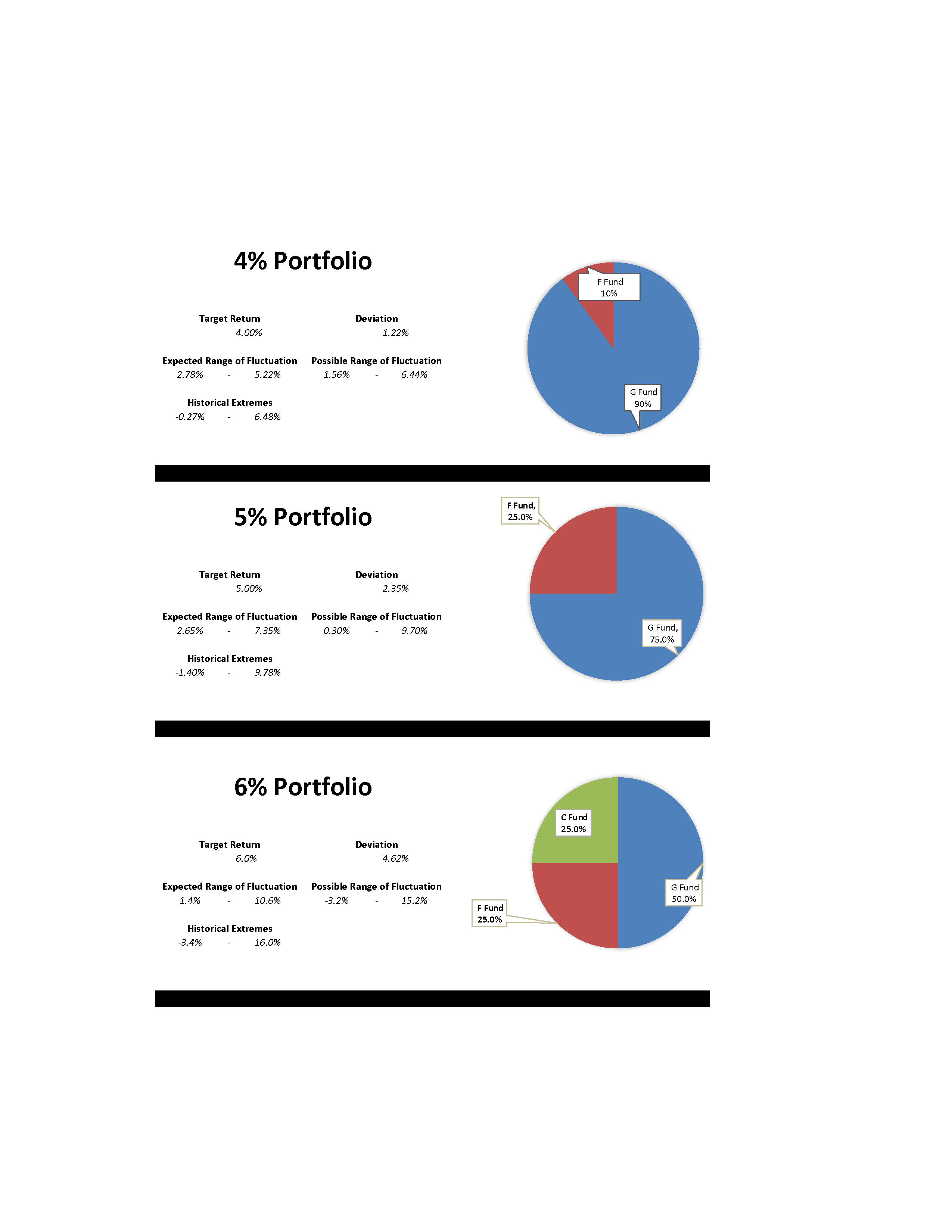

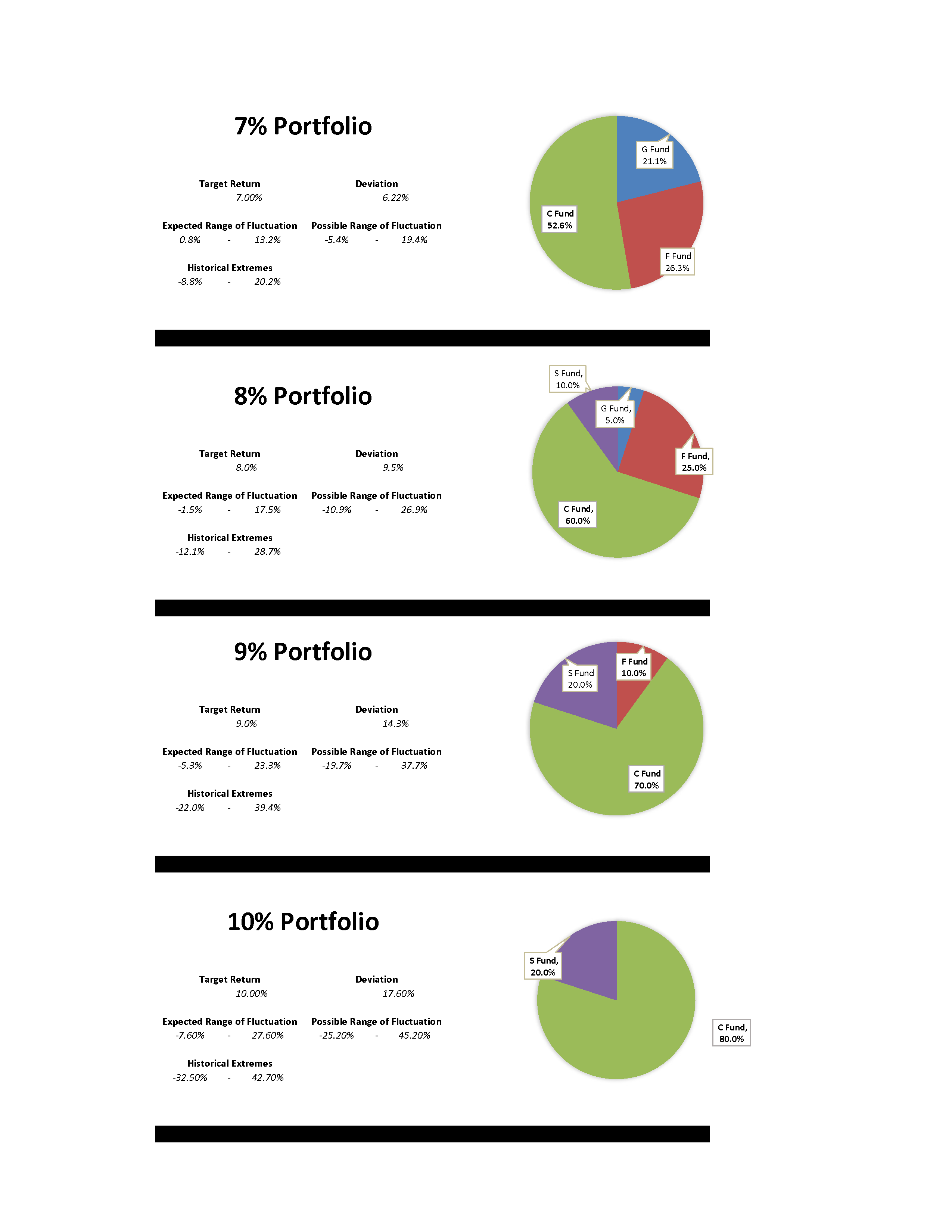

See this month’s portfolios. DON’T JUST LOOK AT RATE OF RETURN. Always view the target return of each portfolio in context of its ranges of fluctuation.

Anyone who has more than 5 years before drawing income from their TSP should consider taking a more aggressive posture going forward and use my aggressive portfolios below. If you are within 5 years of retirement, you should email me to get a more customized recommendation.

If you have any questions, feel free to contact me.

Email me here – stephen@stephenzelcer.com