TSP Planning Report May 2024

Facts:

- The G Fund rate for May 2024 decreased from 4.375% to 4.25%.

- The Fed Funds interest rate remained at 5.3%.

- This month’s unemployment rate decreased to 3.8% from 3.9%.

- The 1st Estimate for Q1 2024 GDP came in at 1.6%. Last quarter’s GDP was 3.4%.

- PMI (Purchasing Managers Index) stalled, reading at exactly 50 (any reading below 50 represents contraction, any reading above 50 represents expansion, a reading of 50 means no expansion or contraction).

- The S&P 500 (C Fund) decreased 4.3% in April 2024. Thus far in 2024, S&P 500 is up 5.81% YTD.

Assessment:

Rising Inflation

For the third month in a row, inflation readings came in higher than hoped, with the most recent reading of 3.5%, which was even higher than March’s 3.2%.

As such, investors feared, rightly so, that the Fed would need to combat inflation by increasing interest rates.

But, as I pointed out in the past 3 month’s report, we are in an election year, and raising interest rates is not a good election campaign strategy. Today, on cue, the Fed announced it will NOT increase interest rates. Who saw that coming?

Rising Defaults:

Real Estate Defaults saw an uptick recently. According to a report by FOX news, commercial real estate foreclosures increased 6% in March. $929 Billion of commercial Real Estate loans are set to mature this year (2024). Borrowers may have no choice but to refinance with significantly higher interest rates or sell their properties at a steep loss.

Here’s an illustration:

A commercial real estate investor may be holding a 4% mortgage from 2018 that is due this year. Their loan matures this year, and they may need to refinance into an 8%+ mortgage. That, by itself, is a challenge. However, it gets worse.

Commercial real estate values have declined. A building that was bought for $10M in 2018, may now be worth $8M in 2024. Assuming a 20% LTV, the loan on that original $10M property was $8M. When it comes time to refinance, if the property is now valued at $8M, the LTV would only allow a loan of $6.4M. That means the property owner needs to somehow find $1.6M of cash just to refinance the original $8M loan.

When confronted with this decision – either cough up another $1.6M and refinance into costly 8%+ loans, or cut your losses and walk away – it’s not hard to foresee many owners walking away from their loans, and defaulting.

However, in the same Fox report referenced above, the Fed is aware of these risks and feels these risks don’t affect large scale banks, but only small, regional banks, which carry 80% of this commercial real estate risk. If the defaults rise, the regional banks may go under, but the national banks are better situated and the Fed feels we are not confronting a 2008 scenario, again.

Bottom Line:

Since the Fed is not expecting to LOWER interest rates, investors may not have as much borrowed money available for investing, and as such may need to access their own cash. This money may need to be drawn out from their stock-market investments and, if done on a national scale, will put downward pressure on the stock market.

There are many arguments to say the market will be pushed downward for the foreseeable future. The only bright spots are:

- It’s an election year, and lowering interest rates is in the interest of an incumbent to boost their re-election bid.

- Companies have a vested interest in making profits. In general, I am confident in the power of companies to make profits, and if they do, the economy will thrive and the market will continue to rise – so long as Governments don’t interfere.

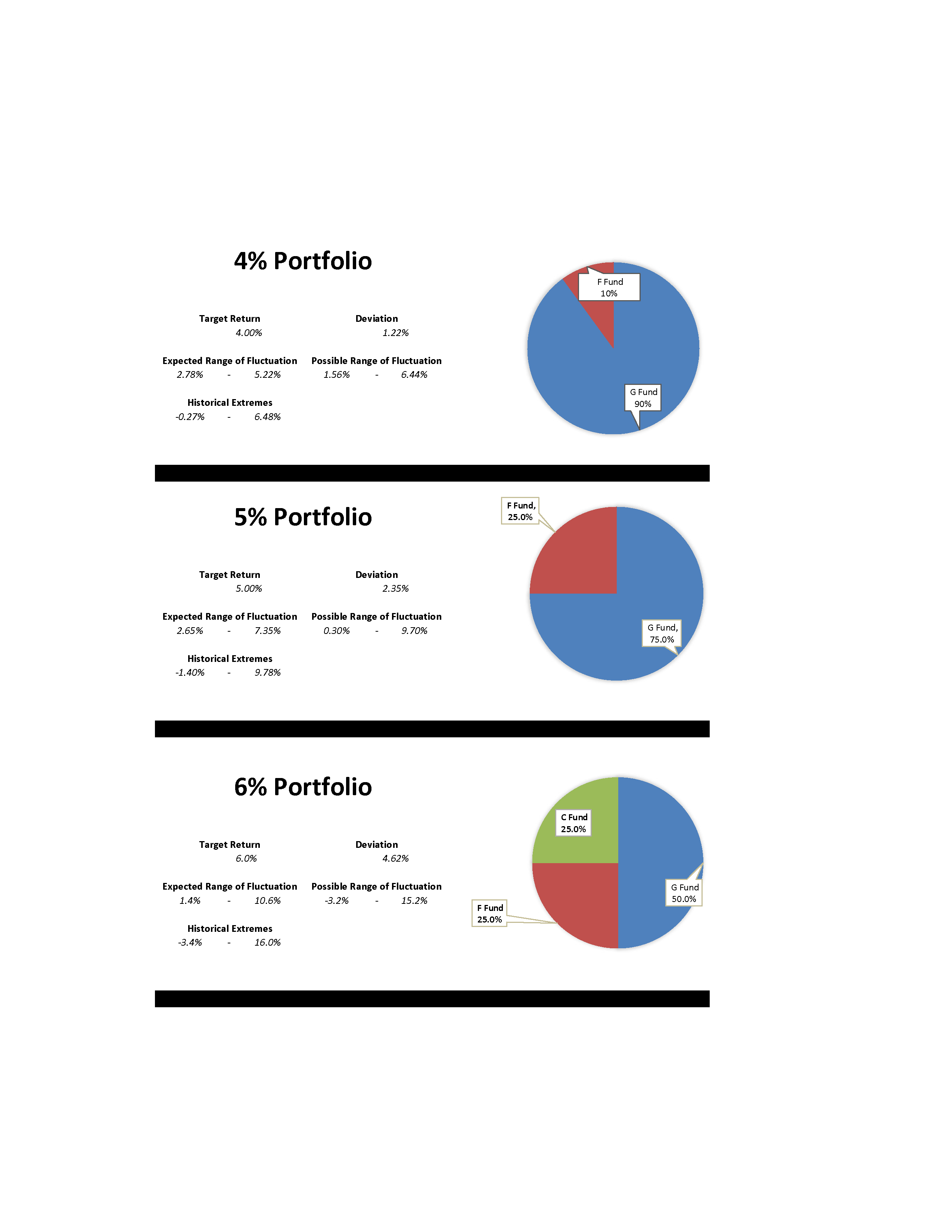

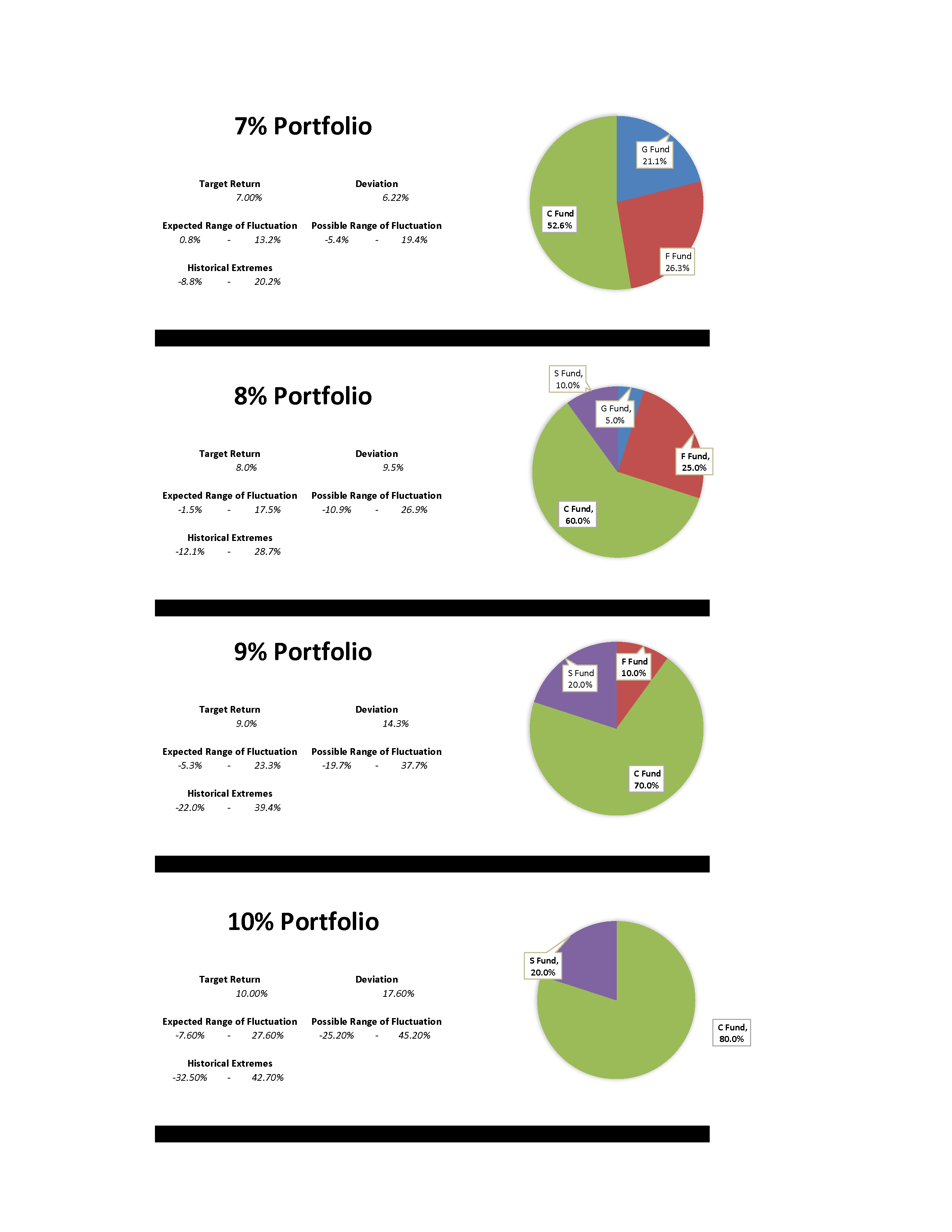

See this month’s portfolios. DON’T JUST LOOK AT RATE OF RETURN. Always view the target return of each portfolio in context of its ranges of fluctuation.

Anyone who has more than 5 years before drawing income from their TSP should consider taking a more aggressive posture going forward and use my aggressive portfolios below. If you are within 5 years of retirement, you should email me to get a more customized recommendation.

If you have any questions, feel free to contact me.

Email me here – stephen@stephenzelcer.com